Education Savings Simplified | Dallas Financial Advisor's Guide to 529 Plans

As a Dallas-based Certified Financial Planner™—and a mom to two amazing girls—I know the emotional weight that comes with trying to plan for your children’s education. Writing the “college chapter” in my book Future Focused Wealth was incredibly meaningful because it made me reflect on what I truly want for my daughters: opportunity, flexibility, and a debt-free future.

The same dreams apply to the families I work with every day in Dallas. Whether your child is still learning ABCs or already applying for college, one truth holds:

Saving early and strategically is one of the most powerful financial gifts you can give your child.

Why Saving for College Is Better Than Borrowing

It’s easy to put off college savings in the hustle of daily life. But here’s what I tell my Dallas clients:

- You can borrow for college, but you can’t borrow for retirement.

- The earlier you start saving, the more power you have over your financial future.

- Every dollar saved now reduces the need for high-interest loans later.

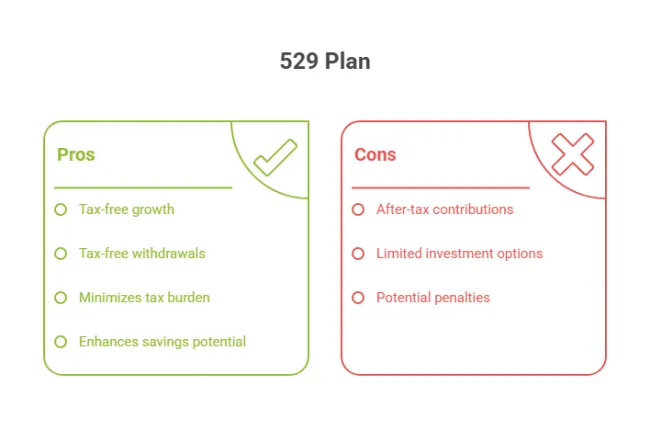

529 plans—and other education savings tools—can offer tax-free growth, flexibility, and control. The key is understanding how they work.

What Is a 529 Plan?

A 529 plan is a state-sponsored investment account designed to help families save for education costs. Its primary benefits include:

- Tax-deferred growth on your contributions.

- Tax-free withdrawals when used for qualified education expenses.

Flexible ownership—parents, grandparents, or other relatives can open or contribute.

What Can 529 Funds Be Used For?- College tuition and fees

- Room and board

- K–12 tuition (up to $10,000/year)

- Trade school or vocational programs

- Graduate school

- Student loan repayment (up to $10,000 per beneficiary)

📌 Dallas Planning Tip: Some clients even use 529 funds to pay for private high school or future graduate degrees. The flexibility is greater than most people realize!

What 529 Plans Can’t Be Used For (Know Before You Withdraw)

While 529 plans offer incredible tax advantages and flexibility, they do come with rules and restrictions. Using the funds for non-qualified expenses can trigger taxes and penalties—something I always help my Dallas clients avoid with smart planning.

Here’s what 529 funds cannot be used for without consequences:

❌ Non-Qualified Expenses That Trigger Penalties:

- Transportation costs (gas, flights, parking)

- College application or testing fees (SAT, ACT, application costs)

- Health insurance premiums

- Extracurricular activity fees (sports, clubs, etc.)

- Cell phones, internet, or non-required tech

- Furnishing a dorm room (decor, bedding, etc.)

- Optional meals or off-campus food (unless part of a campus meal plan)

📌 Dallas Planning Tip: Even if something feels “education-related,” it doesn’t mean it qualifies. The IRS has specific rules—and using 529 funds incorrectly could mean paying income tax + a 10% penalty on the earnings portion of your withdrawal.

How to Avoid Mistakes:

- Stick to school-issued expense statements. If it’s listed on the tuition bill, it’s usually qualified.

- Ask your school’s financial aid office. They can confirm what’s considered a “qualified education expense.”

- Work with a fiduciary CFP® (like me!) who can coordinate your college savings with FAFSA, taxes, and timing.

💬 Fiduciary Insight: I regularly help Dallas families track 529 usage and reimbursements properly—so every dollar works hard and stays tax-free.

Can I Use a 529 Plan for Graduate School or Trade School?”

Answer:

Yes! 529s are not limited to undergrad. You can use them for:

- Law school, med school, MBA programs

- Vocational/trade certifications (e.g., welding, plumbing, cosmetology)

- Study abroad (if the institution is FAFSA eligible)

📌 Dallas Note: I often see families assume a 529 is only useful for 4-year college. That’s a missed opportunity! We can often continue growing the fund or repurpose it for career pivots later in life.

How Much Should You Save—and When Should You Start?

Here’s a general savings roadmap:

🧠 Pro Tip: Even $50/month gets you in the game. Start small, automate contributions, and scale as income grows.

529 Plan Fees, Costs, and Performance

Not all 529s are created equal. Here's what to look out for:

1. Expense Ratios:

Each fund within the 529 plan has a cost, usually ranging from 0.10% to 1.00%. Lower is better, especially if you're in it for the long haul.

2. Administrative Fees:

Some state plans charge annual fees just to maintain the account. Texas’s plan is competitive, but review the plan document carefully.

3. Investment Options:

Most 529s offer age-based (set-it-and-forget-it) or static portfolios. I help clients choose the right fit based on time horizon and risk tolerance.

📌 Dallas Fiduciary Insight: I routinely compare state plans nationwide to find the lowest-fee, highest-performance options—even if they’re outside of Texas. You don’t need to live in a state to use its 529.

Ready to stop guessing and start planning smarter?

👉 Book a call now

Where to Open a 529 Plan: State vs. National Options

One of the most common questions I get from Dallas parents is:

“Do I have to use Texas’s 529 plan?”

The short answer? No.

You can open a 529 plan in any state—and some states offer better investment choices, lower fees, or user-friendly interfaces that make them more attractive.

Comparing In-State vs. Out-of-State 529 Plans:

📌 Dallas Planning Tip: Since Texas doesn’t offer a tax deduction, you’re free to choose any state plan. I often recommend options based on investment performance, flexibility, and fees—not geography.

Where Should You Open a 529 Plan? Direct vs. Advisor-Managed Accounts

One of the most important decisions in setting up a 529 plan—especially for Dallas families—is how and where to open it.

You generally have two options:

- Open a 529 directly through the plan provider (also called “direct-sold”)

- Open it through a financial advisor (often called “advisor-sold”)

Both have pros and cons—and which one makes sense depends on your financial goals, portfolio complexity, and how hands-on you want to be.

Option 1: Opening a 529 Plan Directly (DIY Approach)

Direct-sold 529 plans are opened and managed online, without professional support. You select the state, set your investment strategy, and monitor it yourself.

✅ Pros:

- Lower fees (no advisory fee or commissions)

- Easy online setup

- Age-based portfolios available for simplicity

- Good fit for smaller accounts or DIY investors

❌ Cons:

- No personalized guidance

- Limited tax and financial planning integration

- Easy to underfund, overfund, or miss coordination with FAFSA

- No behavioral coaching or strategy adjustment over time

💬 Dallas Insight: Many families I meet started their 529 “DIY-style” but later realized it wasn’t aligned with their overall financial plan or tax strategy. Small decisions made early—like naming the wrong owner or choosing a too-aggressive portfolio—can have long-term consequences.

Option 2: Opening a 529 Through a Financial Advisor

Advisor-sold plans are opened with the help of a financial planner—ideally a fiduciary CFP®, like in my Dallas practice. These plans may have slightly higher fees but come with strategic guidance.

✅ Pros:

- Personalized savings strategy based on goals, timeline, and income

- Integration with your retirement, estate, and tax plan

- Help navigating gifting strategies (like super-funding)

- Ongoing monitoring, rebalancing, and behavioral coaching

- Help coordinating across multiple children or generations

❌ Cons:

- May involve advisory fees (often under 1%)

- Not ideal if you prefer 100% DIY

💼 Fiduciary Perspective: In my role as a Certified Financial Planner™, I build evidence-based education strategies tailored to your family’s life stage, goals, and financial future.

Which Option Is Right for You?

Cost

📍 Dallas Family Strategy Tip: If you’re just starting out with a small monthly contribution and want to keep it simple, a direct plan may be enough. But if you’re contributing more, coordinating with other goals, or concerned about tax and legacy planning, working with a fiduciary advisor will often pay for itself in value and peace of mind.

Want to explore whether a direct or advisor-managed plan makes the most sense for your family?

👉 Schedule a strategy session

How 529s Are Taxed (and Not Taxed!)

Federal Tax Benefits:

- Contributions grow tax-deferred

- Withdrawals used for qualified expenses are federally tax-free

State Tax Benefits:

- Texas has no income tax, so there's no deduction—but you still get tax-free growth.

Gifting Rules:

- Individuals can gift up to $18,000 per year (or $90,000 using 5-year super-funding in 2025) without triggering gift tax reporting.

Alternatives to 529s

📌 Fiduciary Planning Tip: I often use a hybrid strategy—layering 529s with other tools depending on tax goals and family structure.

What If Your Child Doesn’t Go to College?

Don’t worry—your savings won’t go to waste:

- Change the beneficiary to a sibling, parent, or other family member.

- Use funds for trade school, grad school, or K–12 tuition.

- Thanks to SECURE Act 2.0, you can now roll up to $35,000 from a 529 into a Roth IRA (if the account is 15+ years old and other rules are met).

📍 Dallas Reality Check: I regularly help families repurpose unused 529 funds into multi-generational planning strategies.

Download Your College Money Report™

Real-World Guidance for Dallas Families

In my practice, I help parents and grandparents:

- Choose the right 529 plan (with low fees and smart portfolios)

- Time gifts and contributions for tax efficiency

- Align 529 plans with FAFSA and college aid timing

- Avoid under-saving—or overfunding—a single child’s education

📚 The education chapter in my book was one of my most personal sections to write. I pictured my girls walking across that graduation stage… not burdened by debt, but backed by a plan we built with love and strategy.

Final Thoughts: Start Where You Are. Plan Where You’re Going.

You don’t need to be “wealthy” to build a strong college savings plan. You just need:

- A clear goal

- A flexible strategy

- And a financial planner who puts your family’s future first

📅 Ready to build an education savings plan that doesn’t derail your financial future?

👉 Schedule a 1-on-1 consultation

Education Planning With Purpose

Helping families plan for education isn’t just part of my job—it’s personal. Every time I sit down with a parent or grandparent here in Dallas, I’m reminded of my own journey with my daughters. Like you, I want to give them choices, freedom, and a future without the financial chains of debt.

Education planning doesn’t have to be complicated. It just has to be intentional—and that’s where I come in.

If you’re ready to create a college savings strategy that actually fits your life, your values, and your budget...

👉 Schedule a 1-on-1 planning call with me today

FAQs: Education Savings for Dallas Families

Q: Can 529s be used for private school tuition?

A: Yes! You can use up to $10,000/year per child for K–12 tuition.

Q: What if my child doesn’t go to college?

A: You can transfer funds, use it for another family member, or roll over into a Roth IRA (up to $35,000).

Q: Do 529s affect financial aid?

A: Yes, slightly. Parent-owned 529s count as parental assets (minimal impact). Grandparent-owned 529s should be coordinated carefully.

Q: What are the fees in a 529 plan?

A: Look for low expense ratios (0.10%–0.50%). I help clients avoid high-fee plans that eat into returns.

Q: Are 529s tax deductible in Texas?

A: No—Texas has no income tax. But you still get tax-free growth and withdrawals.